Transformation, Integration and the New Frontier of Monetary Policy - speech by Governor Petr Kažimír at the Central Bank of Uzbekistan

-

Peter Kažimír

![author image]()

Governor - 4 Mar 2026

We live in a world where economic certainties are harder to come by. Fragmentation, rapid technological change and shifting geopolitical realities are reshaping how economies function — and how central banks think about stability, credibility and trust. In such an environment, it matters more than ever to look beyond familiar frameworks and listen to perspectives shaped by different histories and challenges.

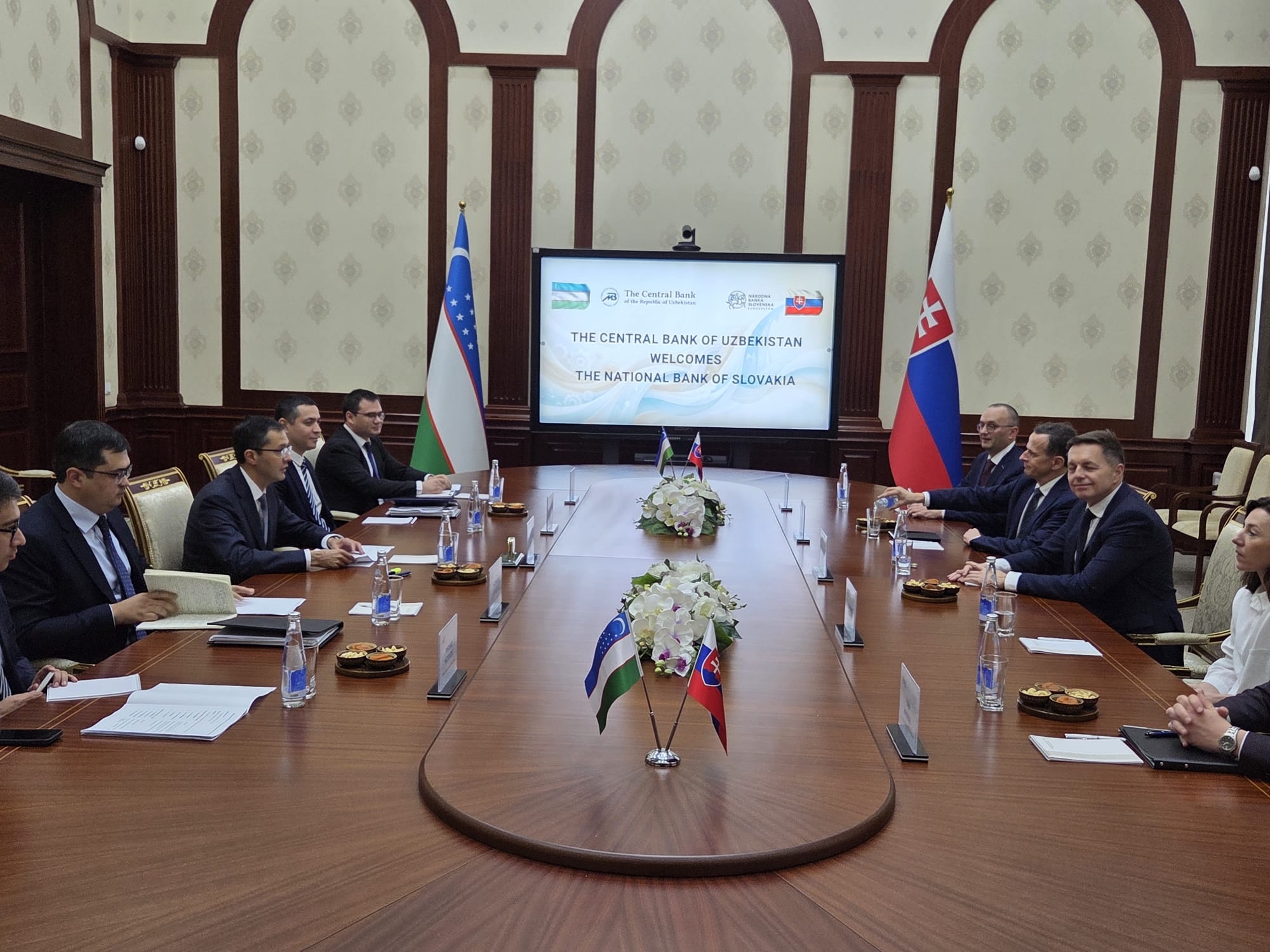

That broader view took Governor Peter Kažimír to Tashkent, where the Central Bank of Uzbekistan became a co‑star in a conversation about transformation and policy in uncertain times. Drawing on Slovakia’s journey from the economic transition of the 1990s to membership in the euro area, the lecture explored how openness, institutional credibility and international cooperation can anchor monetary policy even as the global landscape shifts.

The visit was not only about looking back, but also about looking forward. Together with Governor Timur Ishmetov, discussions focused on deepening cooperation in economic research and technical assistance between the two central banks — a reminder that learning flows in both directions. A highlight was the exchange with young economists and analysts, whose curiosity and sharp questions underscored how much value emerges when different experiences meet.

In today’s complex world, stepping outside our usual policy circles is not a luxury. It is often where fresh ideas emerge — and where central banking’s core mission becomes clearest: building trust and understanding across economies, even as the ground beneath them keeps moving.

The speech:

Transformation, Integration, and the New Frontier of Monetary Policy

Governor, Ladies and Gentlemen, Dear Colleagues,

Let me first thank our hosts for the warm hospitality here in Tashkent.

It is a real pleasure to be here and to exchange views among central bankers—people who know that behind every elegant model stands a very real economy, and behind every decision, real people.

Being here in Tashkent, one is reminded that this has long been a place of exchange—of goods, ideas, and trust—dating back to the time when the Silk Road connected economies across continents.

Today, I would like to share a story of Slovakia’s economic and monetary transformation over the past three decades.

I will not tell you what to do, as every country has its own constraints.

But experiences can travel, and sometimes lessons learned the hard way are the most valuable to share.

1. The Slovak Journey: From Transition to Stability

Thirty years ago, Slovakia was a very different economy.

In the early 1990s, we were emerging from central planning and building basic market institutions from scratch.

Inflation was high, and public finances were fragile. We had to earn our credibility one step at a time.

An early, fundamental lesson was this: macroeconomic stability is not a by-product of growth—it is a precondition for it.

We focused on two main forces: openness and credibility.

Slovakia chose to integrate deeply into global value chains.

By attracting foreign direct investment, we transformed into a global automotive hub.

We currently produce more cars per capita than any other nation, with partners ranging from Volkswagen to our newest addition, Volvo.

However, this growth required a central bank that could act as an anchor.

The National Bank of Slovakia had to evolve from basic tasks like building payment systems to complex mandates involving financial stability.

What we learned is that a central bank’s mandate never stands still.

It must adapt to new risks, but it always requires three pillars: independence, analytical capacity, and public trust.

One specific lesson for any transitioning economy is the importance of the banking sector.

In the late 90s, we had to confront deep weaknesses in our banks decisively.

We learned that problems in banks do not disappear on their own; they must be addressed transparently and early.

Without a healthy banking sector, our monetary policy decisions would never reach the real economy.

2. The Path to the Euro: A Strategy of Discipline

Joining the euro area in 2009 was not a matter of prestige; it was a macroeconomic strategy.

We gave up an independent monetary policy to gain a global currency, lower risk premia, and long-term stability.

I often compare this process to preparing for a long-distance race.

The “medal” of adopting the Euro mattered less than the “training” required to get there.

The discipline forced us to fix our inflation control and fiscal responsibility. We had to convince the public not just that inflation was coming down, but that it would stay down.

Once inside the euro area, the rules changed.

Since interest rates are set for 21 different economies, we no longer ask if a policy is perfect for Slovakia alone.

Instead, we ask how we can adapt on a national scale.

This makes fiscal policy and macroprudential tools our primary instruments.

If the exchange rate cannot move, then prices, wages, and productivity must be flexible enough to absorb shocks.

3. Global Challenges: The “New Normal”

While our histories differ, we now face a global environment that is changing faster than before.

Leading central bankers, such as the FED’s chair Jerome Powell and BIS Pablo Hernández de Cos, have recently highlighted that we are operating in a more constrained world.

The “Last Mile” of Inflation

After years of low inflation, its sudden return reminded us why credibility is our most important asset.

In Slovakia, inflation peaked above 15% due to energy shocks.

Tightening policy was unavoidable. As Chair Powell has noted, there is “no risk-free path” in the final stages of fighting inflation.

If we ease too early, inflation returns; if we ease too late, we hurt the economy. The lesson is clear: delaying action is often more costly than acting early.

Uncertainty and the Neutral Rate

We are also facing uncertainty regarding the “neutral” interest rate—the rate that neither stimulates nor restricts the economy.

Because the old economic maps no longer apply, we must be “data-dependent.”

We cannot rely solely on pre-pandemic models; we must monitor how the economy responds to our moves in real time.

Supply-Side Shocks and Fragmentation

We are moving from an era of “just-in-time” global trade to “just-in-case.”

Fragmentation in trade and more frequent supply-side shocks—from energy spikes to climate events—mean that inflation will likely be more volatile in the future.

This is the “New Normal” for all of us.

4. Lessons for the Future

As Uzbekistan continues its journey of modernisation and inflation targeting, I offer three reflections:

- Macroprudential Essentialism: Monetary policy cannot solve every problem. In Slovakia, we use targeted tools—such as capital buffers and borrowing limits—to manage local credit risks without changing the overall interest rate.

- Fiscal-Monetary Alignment: As a former Finance Minister, I know that monetary policy works best when the government is responsible for its budget. In a world of high debt, central banks must remain firm on price stability.

- Communication as a Pillar: In times of high uncertainty, clear communication is a policy tool. It is about anchoring the public’s expectations so they trust that their money will hold its value.

Conclusion

Transformation is not a single moment… it is a continuous process.

Slovakia’s journey shows that there are no shortcuts; consistent, credible policies compound over time to create prosperity.

I began by recalling the Silk Road, which connected economies through trust.

Today, our central banks play a similar role.

We provide the monetary foundation of trust that allows our nations to grow and cooperate in an uncertain world.

Thank you for your attention, and I look forward to our discussion.

Photogallery

National Bank of Slovakia

Communications Section

Imricha Karvaša 1, 813 25 Bratislava

Contact: press@nbs.sk

Reproduction is permitted provided that the source is acknowledged.