SEPA Credit Transfer

The Single Euro Payments Area (SEPA) allows customers to make cashless euro payments to anywhere in the European Union, as well as several non-EU countries, in a quick, safe and efficient way, just like national payments. By increasing competition between providers of payment services and payment card services, SEPA has benefited consumers and firms, who now have a broader choice of payment services driven by technological innovation.

Map legend

Consumers and firms can make cashless euro payments within one SEPA country or between different SEPA countries and these payments are subject to the same conditions, rights and obligations regardless of the SEPA country in which the payment account is held.

SEPA payments can be made through SEPA payment instruments, i.e. SEPA credit transfers and SEPA direct debits, or through payment cards.

Useful links:

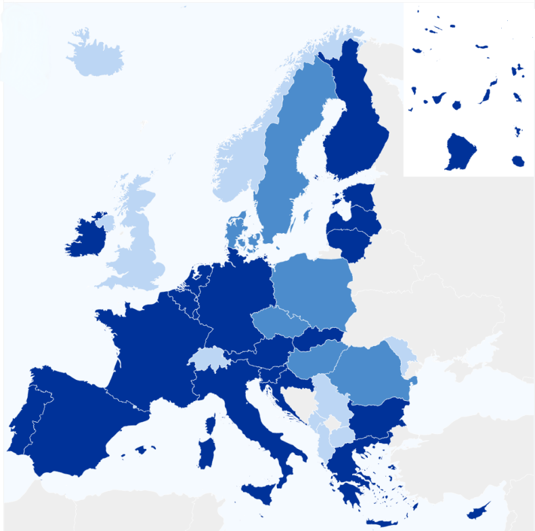

The SEPA region, in which harmonised payment standards apply to cashless euro payments, currently consists of 41 countries, i. e. 27 EU member states, three EEA countries and 11 non-EEA countries. However, the legislation governing SEPA applies only to EU countries.

SEPA countries

- 27 European countries, plus

- Iceland

- Norway

- Liechtenstein

- Albania

- Andorra

- Moldova

- Monaco

- Montenegro

- North Macedonia

- San Marino

- United Kingdom of Great Britain and Northern Ireland

- Serbia

- Switzerland

- Vatican City State

SEPA credit transfers (SCTs) and SEPA direct debits (SDDs) were introduced in 2008 and 2009 respectively. For euro area countries, the SEPA migration end-date was 1 August 2014, while for non-euro area EU countries, it was 31 October 2016.

As of these dates national credit transfers and direct debits were replaced by SEPA payment instruments.

In Slovakia, all credit transfers, including domestic transfers, have been processed as SCTs since 1 January 2014, and all direct debits have been processed as SDDs since 1 February 2014.

SEPA credit transfers (SCTs)

A credit transfer is a payment initiated by the payer. The payer gives a payment order to its payment service provider (PSP), for example a bank. The payer’s PSP then transfers the funds to the beneficiary’s PSP. The implementation of SCTs included converting bank account numbers to the IBAN format for all credit transfers and direct debits.

Useful links:

European Payments Council (EPC)

The legislative framework for SEPA is laid down by Regulation (EU) 260/2012 establishing technical and business requirements for credit transfers and direct debits in euro and amending Regulation (EC) 924/2009.

A further legal basis of SEPA payments is provided by the Second Payment Services Directive (PSD 2) which is transposed into Slovak law by Act No 492/2009 on payment services.