Financial Stability and Climate Change

Climate change brings with it both physical risks and risks associated with the transition to a more sustainable model of economic activity. Both groups of risks impact financial markets’ developments and overall financial stability.

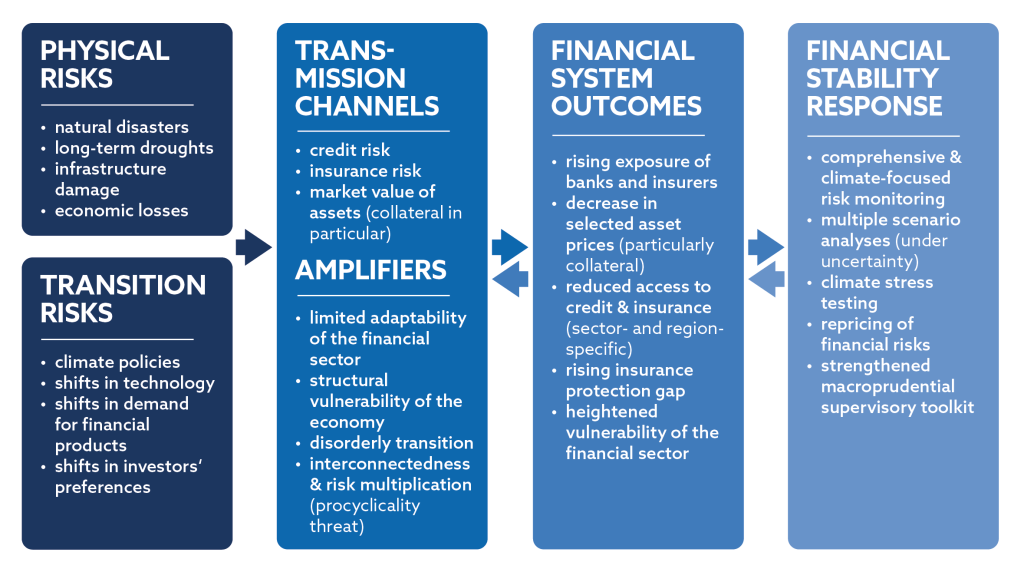

Physical Risks

Physical risks — such as extreme weather events like floods or torrential rains, as well as rising temperatures or prolonged droughts — often lead to economic losses. A decline in the value of assets, collateral, or the productivity of affected sectors can subsequently affect financial market developments through various channels. If these phenomena become more intense or frequent, they can have broader, systemic consequences on both credit and insurance availability and ultimately affect overall financial stability.

Transition Risks

At the same time, the transition to a low-carbon economy is expected to bring significant structural changes across the entire economy. So-called transition risks affect primarily carbon-intense sectors, such as fossil fuel production and processing, energy, heavy industry, and transportation; and are believed to induce broader asset revaluation. Changes in supply chains as well as in investment portfolios’ composition are likely to follow.

Given the content of climate policies already adopted or those under development, it can be expected that production costs in these sectors will gradually rise.

The question therefore remains to what extent companies in sectors concerned will be able to maintain their competitiveness and profitability amid increasingly stringent regulations.

Their ability to repay liabilities in tightened conditions might be questioned as well.

Economic and Financial impacts of Climate Change

Thus, both groups of risks — physical and transitory — can thus cause losses at the level of banks, insurers, and financial markets, thereby affecting financial stability.

The NBS, contributing to the stability of the financial system and also serving as the supervisory authority for the banking, insurance, and capital markets in Slovakia, takes these risks into account and is gradually incorporating them into its core operations. It assesses the financial market’s resilience to climate risks, for example, by conducting stress tests and expanding the financial reporting framework for financial market entities. More detailed reporting will provide the NBS with a better overview of financial sector’s exposure to climate risks, thereby strengthening the data foundation for potential future regulatory decisions. Based on previous comprehensive assessments, though, the NBS confirms that climate risks do not to pose a direct challenge to financial stability in Slovakia.